Despite the Covid-19 pandemic, the fintech industry continues to thrive and innovate. With this being said, Akoni participated in the Future of Open Banking panel with Innovate Finance and moderated by Tram Anh Nguyen from CFTE (Centre for Finance, Technology and Entrepreneurship) as part of UK Fintech Week. I was fascinated to see strong attendance of 600 participants from across the globe. The range of questions from the audience demonstrate that we are at the start of an exciting journey, with transformative benefits to customers.

At Akoni we see even more of these benefits during the time of Covid-19 as a global crisis, using tools to help across all segments of society - from small businesses to charities and individuals, through our partner distribution clients.

We participated with market leaders Samantha Seaton from MoneyHub, Ross Laurie from Visible Capital, Emily Reid from Hogan Lovells, David Beardmore from Open Banking and Chris Gorst from Nesta and are reflecting on some of the shared thoughts below.

Open Finance: What is the Future of Open Banking?

- Open Banking surpassed 1 million users in January this year and continues to grow. Read more here.

- Consumers can view all accounts in one place and have various benefits used by B2B2x channels, where businesses and individuals benefit from automating account opening and ease of use.

- Clients are now demanding increased services around their finances - in addition to banking - to connect insurance, pensions, savings, debt and mortgages as well as property values. On the business side, similarly there is increased demand for simpler processes and personalised product prompts, with simultaneous delivery of the relevant financial product. Customer demand is driving change as well as driving more large scale corporates and financial institutions to transform their service delivery to clients.

Benefits of Open Banking and Open Finance:

- Personalised products for your stage of your life or your business life cycle with real-time updates due to market or your own changes.

- Faster decision making particularly during times of crisis such as Covid-19.

- Using tools such as Open Banking for anti money laundering/KYC process - all from your sofa, made more relevant during times of lockdown and remote working. Open Banking enables simple bank account access and verification and together with our on-boarding tools provide a 5 minute AML/KYC process.

- Democratising near real-time investment and savings decisions, essentially providing what was previously only accessible to global multinational corporates with treasury teams. Now data, technology and banking partnerships enable delivery of this in a controlled and large-scale manner.

- Using value- based drivers such as ESG/environmentally and socially friendly funds, and risk drivers including spreading risk across multiple banks, using various data sources, such as Akoni providing Fitch Financial implied ratings by Fitch solutions and using tools to protect cash by spreading across multiple banks.

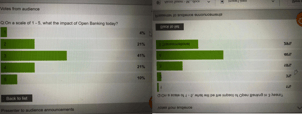

As can be seen from the before and after poll, we all anticipate transformation to have a material impact over the upcoming 3 years.

Our panel saw a range of interesting questions which we covered, and some noted below where we did not have time to cover:

- How quickly do you think that open banking concepts are going to spread and become harmonised globally (as I understand it, beyond Europe there are only a handful of countries around the world building open banking frameworks)?

This has been happening in the US for years with safety-checks (automatic transfers from savings to checking to cover overdrafts as an alternative to credit-line over drafts. Open Banking is all but obsolete in the US with Venmo & Zelle (the clearXchange network the big four banks created years ago well ahead of the curve. Plaid-like portals are useful but already established and now sold to Visa. Open Banking seems quite idealistic when there are use-cases using existing proprietary products.

- What would your advice be for FS companies to balance operational resilience and innovation as open banking / finance adoption continues to accelerate?

Collaboration is key to initiatives to drive the adoption of Open Banking. Customers do not see an Open banking tool - they simply see a tool provided by a trusted financial institution which gives benefits, eg. increases their income, provides quicker decisions on credit, or makes it easier to move money around while providing prompts and recommendations for spending. There are 2 types of collaboration:

- Fintechs such as Akoni working with Banking partners, IFAs, wealth platforms and insurers - deploying our technology on a white label branded portal or through a fully integrated API solution.

- Fintechs working collaboratively together to deliver improved solutions for clients.

3. The insurance market has started to use various open banking and open data tools in different ways already. The pensions market and employee benefits has emerged from the traditional insurance sector and is responding with white label tools. We are seeing this increase to adviser and wealth platform offerings. In addition business insurers are growing further.

The insurance market has started to use various open banking and open data tools in different ways already. The pensions market and employee benefits has emerged from the traditional insurance sector and is responding with white label tools. We are seeing this increase to adviser and wealth platform offerings. In addition business insurers are growing further.

Adoption will be driven by benefits including collaboration, personalised products and the use of innovative tools like Open Banking. As customers see the use of new technology and tools, in a safe and trusted way.

4. Hi, thanks for all the invited speakers in this interesting webinar subject. My question focused on the core subject of this talking "open finance and open banking", so does this mean that banks are not open enough in their strategies against market volatility and future client needs? However, what are the probable potentials of collaboration among the new fintech startups and the big known banks that were opened to the market change?

Many other questions were raised such as:

- Do you see any proven success stories for a win win business models ? Where both the banks and the fintechs gain from this implementation? In terms of revenues or cost return on investment.

- How better off are consumers and businesses financially since open banking? Have we seen quantitative data showing it has been beneficial?

- What influence of re-building trust post 2008 have the panel witnessed in harnessing customer use of OB/OF? Are you exploring garnering trust to propel OB/OF to the transformational level?

- Do you see any changes of the customer behaviour / Open banking environment given the current situation (i.e. COVID)?

- Does the consumer trust a consumer brand enough to deliver a financial service? Is this a barrier for open finance to deliver outside of financial service businesses?

- When will payment initiation data benefit the end user. it must be more than the SCA delay.

Clearly we are in a climate of rapid change driven by Open Banking and Open Data. We are always available to discuss where we see changes and how Akoni and our partners can help with this - as part of current Covid-19 response here as well as being part of the SME Finance taskforce here. We are committing to collaborating and delivering benefits across the market to all our clients and partners. Please contact us for a further discussion.

About Akoni: Akoni is an award-winning UK cash platform, which provides a marketplace to SMEs and charities, as well as to individuals through our white label distribution partners including IFAs, wealth platforms, accountants and SME hubs. Akoni uses innovative technology to personalise cash planning solutions for clients, and also provides a full API solution to banks and insurance clients.

Contact us contact@akonihub.com and Find out more www.akonihub.com and www.akonitech.io